LPs to GPs: It’s Time to Deliver

27 July 2023According to key findings from the SS&C Intralinks 2024 LP Survey, a clear message is being sent to fund managers by LPs: They want to invest more but expect strong performance. How should GPs respond?

Volatility in the public markets. A macro environment of higher interest rates. Ongoing turbulence in geopolitics. Against this backdrop, and following the worst year for the 60/40 portfolio of stocks and bonds in decades, investors are increasing their allocations to alternative investments that are focused on private markets.

That is one of the main findings in the SS&C Intralinks 2024 LP Survey, produced in association with Private Equity Wire, which gathered insights from 251 limited partners (LPs) based globally on a range of topics, including their allocation plans for the next 12 months and current sentiment toward general partners (GPs).

According to our survey, LPs are sending fund managers a clear message: We want to invest more but will hold your feet to the fire.

An age of alternatives may well have arrived — and GPs will need to deliver.

First, the good news for fund managers. Only nine percent of LPs plan to reduce their exposure to alternatives in the next 12 months.

Nearly half (48 percent) of LPs surveyed are planning an increase, with over a third (34 percent) of respondents aiming to expand their exposure by at least 10 percent, slightly higher than a year ago.

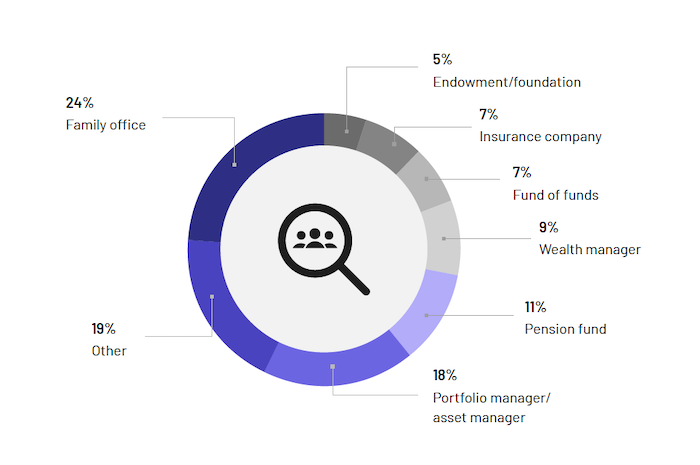

The survey measured the sentiment of a range of professionals who work in the private markets, led by family office allocators, representing 24 percent of respondents.

The views of portfolio and asset managers, pension funds and wealth managers were also well represented, with the vast majority (82 percent) based in Europe, the Middle East and Africa (EMEA) or North America.

Our research indicates that LPs are continuing to look to alternative assets to deliver the risk-adjusted returns and diversification they require. But GPs are facing a challenge to satisfy LPs, with levels of dissatisfaction over performance almost three times higher this year compared to last.

Almost a quarter (23 percent) said performance in alternatives failed to meet expectations, up from eight percent last year.

LPs have thrown down the gauntlet to GPs. Even after a year in which stocks and bonds were sold off in unison, taking big chunks out of conventional portfolios, investors will not be satisfied by mediocre returns or flat performance. The LPs we surveyed want investments in alternatives to deliver strong returns to offset public market losses in turbulent periods. For GPs, this means that there is no room for complacency.

Where was LPs’ satisfaction highest? Private equity continued to deliver strong performance, with more than half (51 percent) of LPs acknowledging it as the asset class that delivered the best risk-adjusted returns.

The nature of opportunity is changing too, as 68 percent of LPs reported being offered opportunities to invest in a GP-led secondary or remain in a continuation fund over the past 12 months. Change continues to be a watchword as does valuation. The recent decline in private equity valuations has had a major impact on investor sentiment, according to the research. It was a key worry in this year’s LP Survey, with 91 percent saying they were concerned about this issue.

A large majority of LPs (81 percent) also expressed concern about banks pulling back from lending on buyouts.

(Above) The 2024 SS&C Intralinks LP Survey measured the sentiment of a range of professionals who work in the private markets. Source.

The rise of private credit

LPs see the best performance in private equity, but the most opportunity in private credit. A vast majority of respondents (71 percent) believe that private credit funds will have a significantly greater role to play in the industry.

The growing enthusiasm for the approach, fueled by alternative credit providers looking to capitalize amidst a period of rising interest rates, is currently seen across the financial landscape.

Forty-two percent of respondents to BlackRock’s recent family office survey were planning a higher exposure — double the 21 percent planning increased allocations to hedge funds.

Marc Pilgrem, the U.S. firm’s EMEA head of family offices, said private credit was “drawing big interest in this higher-rate environment.”

Jason Thomas, Carlyle’s head of global research and investment strategy, called private credit the only game in town, while the University of California’s investment fund will stop betting on hedge funds in favor of private credit.

“Within two or three years, whenever we can get liquidity from our hedge funds, we will be primarily all out,” said University of California CIO Jagdeep Bachher at an investment meeting earlier this year, calling private credit “a better place to be.”

Aside from performance and preference, our research also revealed investor sentiment on a range of other issues, from technology to environmental, social and corporate governance (ESG). LPs also expressed a desire for improvement in the realm of ESG investing.

Respondents were also concerned about GP technology, specifically related to security and reporting. While data security and governance measures emerged as the areas of least satisfaction, “disparate LP dashboards with multiple logins” was the biggest frustration for more than half of LPs (53 percent), an increase from 35 percent last year.

Meanwhile, almost two-fifths (38 percent) of LPs were considering using technology to aggregate data across their private markets portfolios.

2024 LP Allocation Plans

This year’s survey revealed the extent of LPs’ enthusiasm for alternatives — but made clear that GPs have their work cut out for them when it comes to satisfying LPs’ expectations.

Five times as many LPs plan to increase, as opposed to reduce, their 2024 allocations to alternatives (48 percent versus nine percent. But the rate of dissatisfaction over performance is three times higher, even after such a cataclysmic year for 60/40.

Allocators should make sure their commitment to private markets is justified by higher returns. Private equity has been delivering returns, but it is a dynamic picture in which continuation funds are rising in prominence.

Private credit is seen as a big opportunity for many. Future surveys will reveal the ability of GPs to meet LP demand and deliver the strong risk-adjusted returns required.

Alternatives are rising up the agenda and must continue to prove their worth on an annual basis as public market underperformance cannot be counted on in the long run. Allocators will continue to seek maximum value from alternative investment portfolios.

Download the 2024 SS&C Intralinks LP Survey here.

Related Content

Meghan McAlpine

As Sr. Director of Strategy and Product Marketing for Intralinks, Meghan McAlpine is responsible for the go-to-market strategy and driving the growth of the company’s Alternative Investments solution, the leading communication platform for private equity and hedge fund managers and investors.

Prior to joining Intralinks, Meghan worked in the Private Fund Group at Credit Suisse. While at Credit Suisse, she raised capital from institutional and high net worth investors for domestic and international private equity firms.